如何处理营业前费用like pro...

如何处理营业前费用like pro...

如何处理营业前费用like pro...

一般上, 公司营业前所产生的费用都是无法扣税的...

但是...

1. 含义- 营业前的费用

营业前的费用 (Preliminary Expenses/Pre-Operating Expenses)

在公司开始运作之前有些费用是务必要花的,这些费用在会计的角度就是营业前的费用。

这些费用基本包括(并不是每个费用将获得扣税资格):

· 市场调查与研究费用

· 律师与秘书费用

· 公司成立的专业的咨询费用

· 招聘与培训员工的费用

· 行政费用等等

2. 复式进账法

Debit 营业前的费用 (Income Statement - Expenses)

Credit 现金 (Balance Sheet - Current Asset)

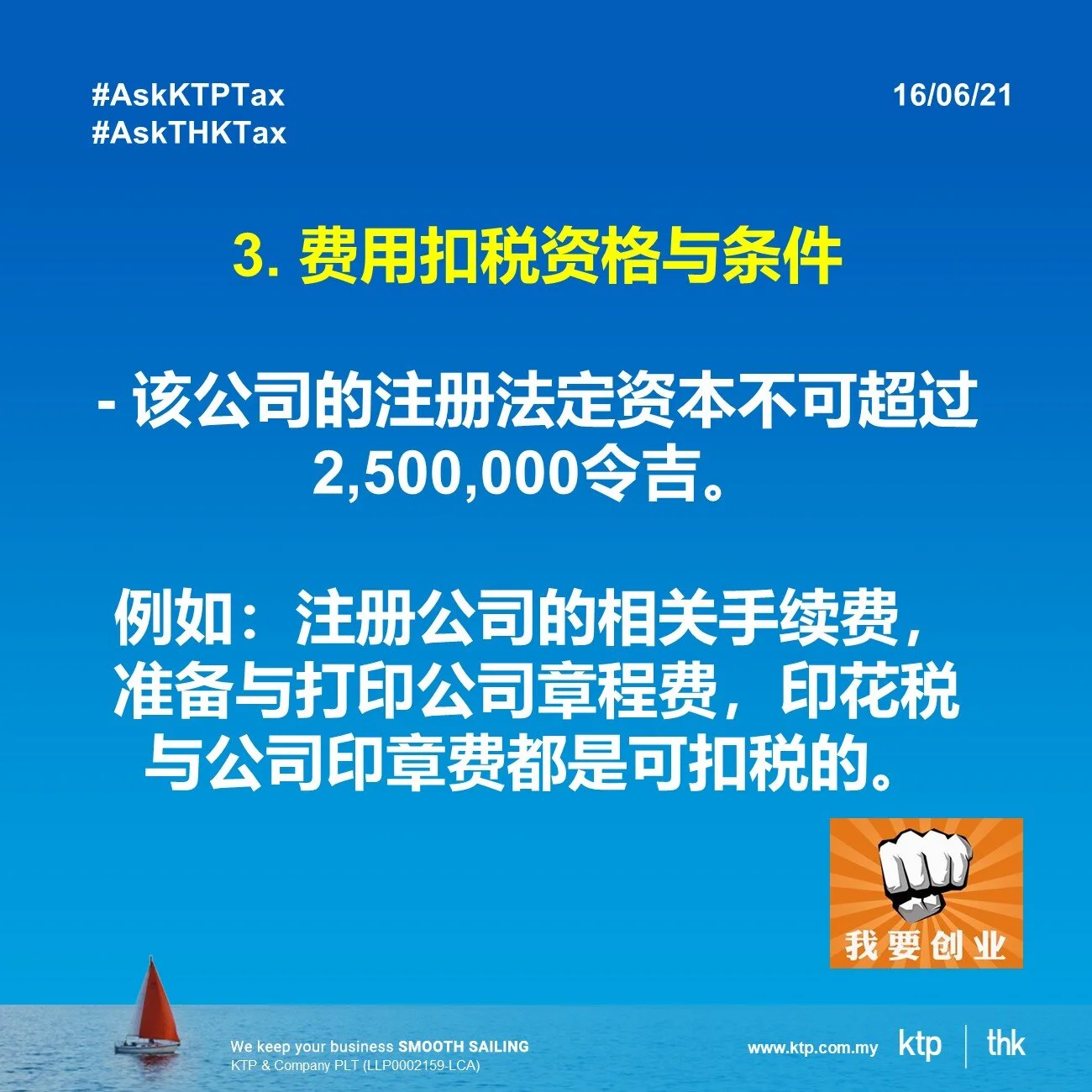

3. 费用扣税资格与条件

一般上,公司营业前所产生的费用都是无法扣税的。但是某些费用在一定的条件下是可以扣税的。条件如下:

- 该公司必须成立与坐落于马来西亚,商业活动也必须获得财政部长的批准。

例如:市场调查与研究费用,以市场调查为目标的国外交通费与每日不超过四百令吉的国外生活花费都能扣税。

- 该公司的注册法定资本不可超过2,500,000令吉。

例如:注册公司的相关手续费,准备与打印公司章程费,印花税与公司印章费都是可扣税的。

- 生产业公司培训员工的费用可享有双重扣税的福利,但必须达到以下条件:培训费须在营业前发生,培训内容须与产品未来的生产相关,培训计划的机构须获得马来西亚工业发展局(MIDA)与财政部长的批准,培训的员工必须是马来西亚公民。

4. 例子

陈先生于2020年2月15日在马来西亚注册成立,法定资本为500,000令吉。他于2020年4月1日开始从事汽车零件零售业务,并于每年的3月31日作为年度结账。截至2021年3月31日, 该公司的营业前费用有:申请生意上的准证,文书注册,公司章程备忘录及印花税。这些费用总共是4,500令吉。

复式进账法:

Debit 营业前的费用 - 4,500令吉

Credit 现金 - 4,500令吉

这些费用在税务上可进行扣税,原因是这些费用属于可扣税费用与法定资本少于2, 500,000令吉。

欲知更多可参考以下网址:

IRB Public Ruling - PRE-OPERATIONAL BUSINESS EXPENDITURE PUBLIC RULING NO.11/2013

http://phl.hasil.gov.my/pdf/pdfam/PR_11_2013.pdf

Visit us

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

Website www.ktp.com.my

Instagram https://bit.ly/3jZuZuI

Linkedin https://bit.ly/3sapf4l

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

Tiktok http://bit.ly/3u9LR6Q

Youtube http://bit.ly/3ppmjyE

Facebook http://bit.ly/3ateoMz

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

Instagram https://bit.ly/3u2PxHg

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

Website www.thks.com.my

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

Archive

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- November 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016