ISQM 1 Audit Risk Assessment

ISQM 1 Audit Risk Assessment

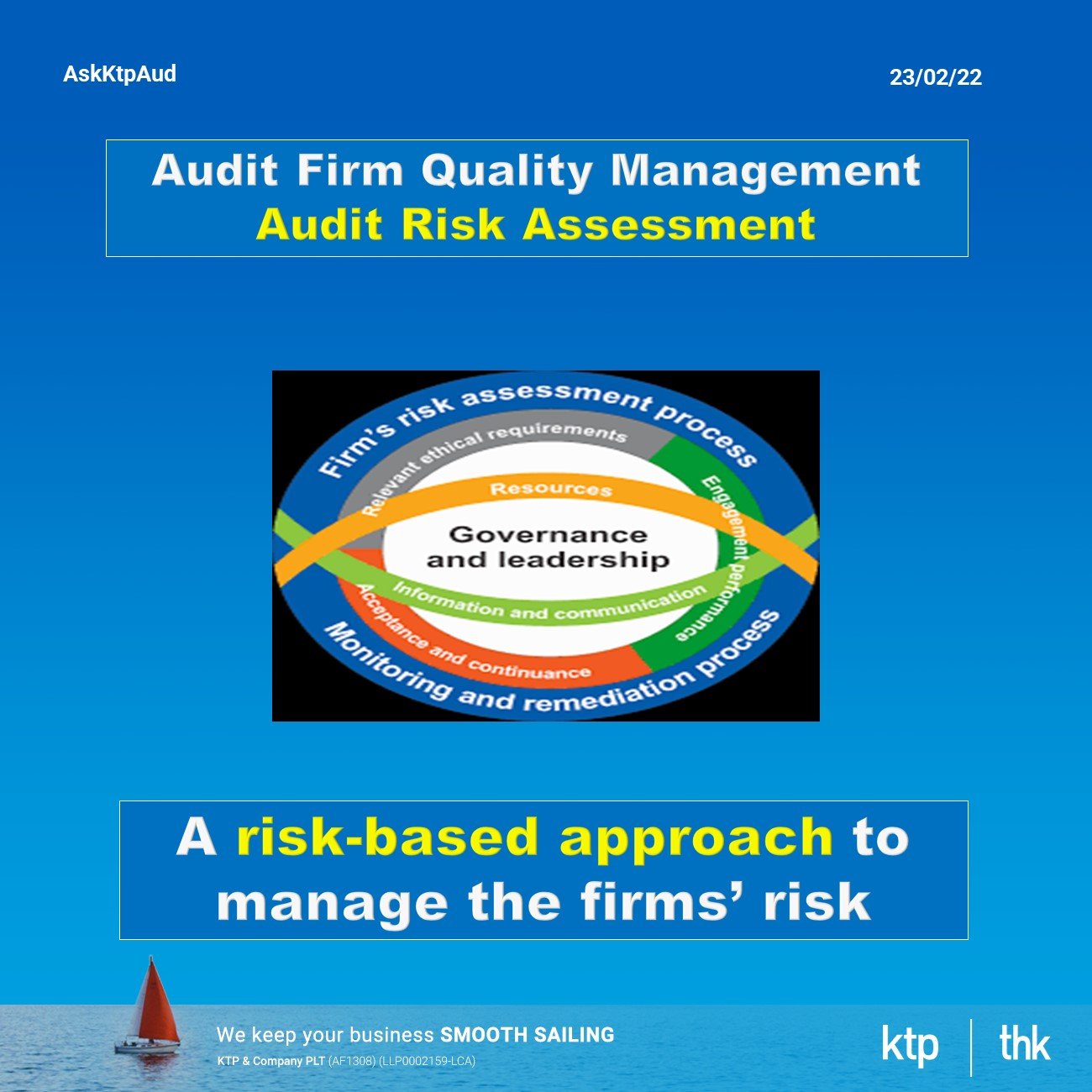

The foundation of ISQM 1, and a key change from extant ISQC 1, is that the firm needs to follow a risk-based approach to quality management, which focuses the firm on :

The firm’s risk assessment process is new to ISQM 1.

• The risks that may arise, given the nature and circumstances of the firm and the engagements it performs; and

• Implementing responses to appropriately address those risks.

A risk-based approach helps the firm tailor the SOQM to the firm’s circumstances, as well as the circumstances of the engagements performed by the firm. It also helps the firm effectively manage quality through concentrating on what matters most given the nature and circumstances of the firm and the engagements it performs.

ISQM 1 requires the firm to have a risk assessment process, the purpose of which is to establish quality objectives, identify and assess quality risks and design and implement responses to address the quality risks.

3 main steps

In designing the quality management system, there are three main steps :

(i) Establish quality objectives to achieve the objective of the system of quality management;

(ii) Identify and assess quality risks to provide a basis for the design and implementation of responses;

(iii) Design and implement responses to achieve those quality objectives.

Quality objectives

The quality objectives are outcome-based to manage quality through the identification of risks. These objectives are established to address possible quality risks that may result in non-quality engagements. For example, insufficient work performed for planning may result in inappropriate identification of audit risks and other significant audit issues.

ISQM 1 specifies quality objectives that firms need to establish, and these objectives are mandatory to be adopted by firms, where applicable. For example, the quality objective of assigning roles and responsibilities for the system of quality management within the firm may not be relevant for a sole practitioner.

In addition to those prescribed by ISQM 1, firms will also need to consider if additional quality objectives are required to be established based on the firms’ risk assessment processes, where applicable.

Quality Risk

One of the new requirements of ISQM 1 is the identification of quality risks with respect to the nature and circumstances of the firms and their engagements. For example, the complexity and operating characteristics of the firm, management style of leadership, client portfolio and complexity of the engagements performed by the firm will impact the risk assessment process and result in different quality management systems for individual firms.

There are no prescribed quality risks in the standards. Firms are required to obtain an understanding of the conditions, events, circumstances, actions or inactions that may adversely affect the achievement of the quality objectives with respect to the nature and circumstances of the firms and their engagements prescribed in paragraph 25(a) of ISQM 1, with the caveat that the list is non-exhaustive.

Firms are expected to identify their own quality risks, assess if a risk has a reasonable possibility of occurring, and how the risk may adversely affect the achievement of one or more quality objectives when it occurs, either individually or in combination with other risks.

Responses

Once the quality objectives and their quality risks have been established (other than some responses specified in the standard that firms are required to design and implement), firms are expected to develop their own responses to address the identified quality risks.

It is also important to take note of the interconnectivity of different components, such as, ethics-related requirements are being dealt with in the information and communication component, as well as the relevant ethical requirements component.

The responses to common quality risks identified by different firms may differ as each firm is faced with varying conditions, events, circumstances, actions or inactions.

Hence, firms will need to customise the design, implementation and operation of their quality management systems to ensure that they are responsive to changes in the nature and circumstances of the firms and their engagements.

The next few sections will illustrate the key principles of the remaining components with an example of quality risk and the proposed corresponding response.

Visit Us

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

Website www.ktp.com.my

Instagram https://bit.ly/3jZuZuI

Linkedin https://bit.ly/3sapf4l

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

Website www.thks.com.my

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

Tiktok http://bit.ly/3u9LR6Q

Youtube http://bit.ly/3ppmjyE

Facebook http://bit.ly/3ateoMz

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

Instagram https://bit.ly/3u2PxHg

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Archive

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- November 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016