How do you audit the opening balance for initial engagement?

How do you audit the opening balance for initial engagement?

Overview

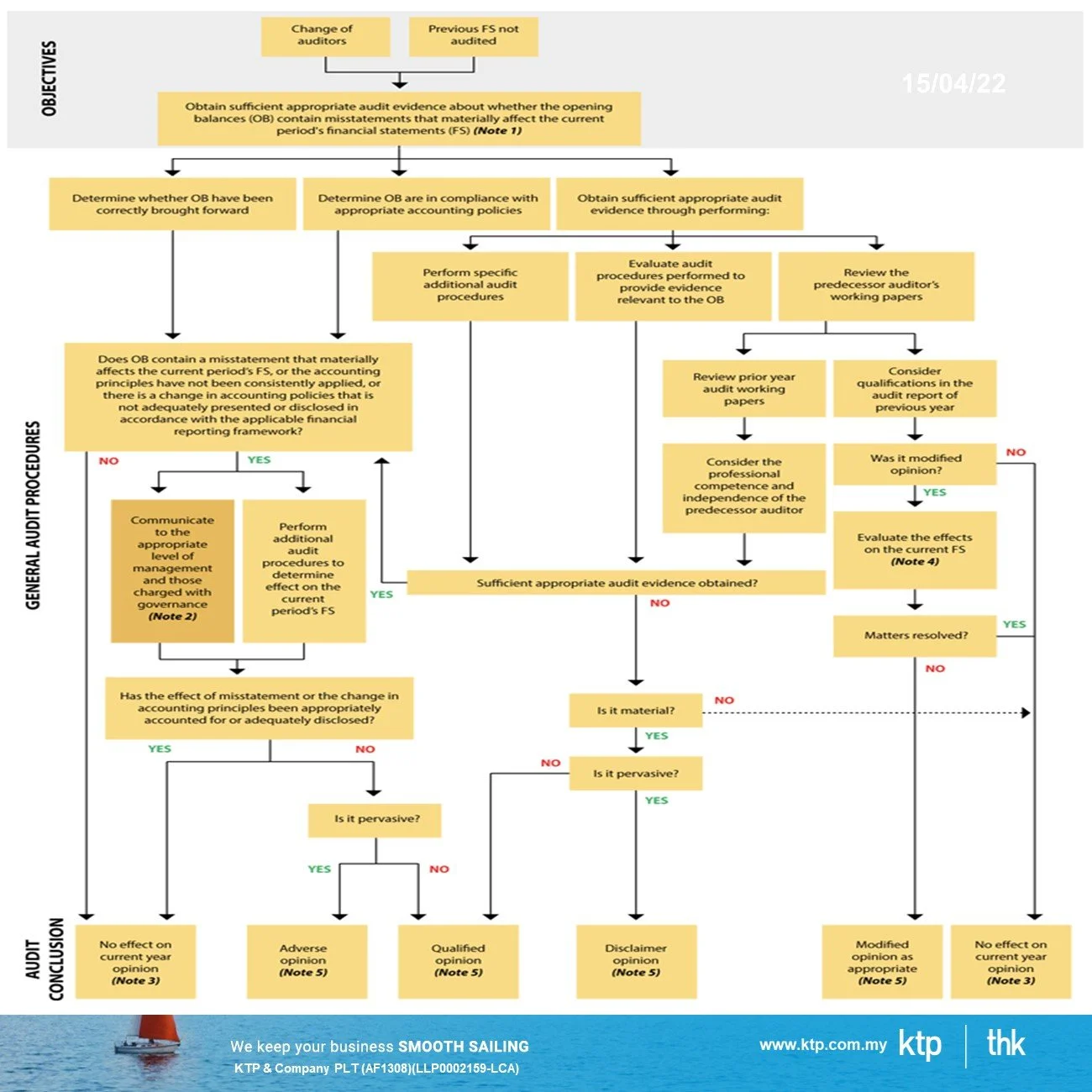

The responsibilities and requirements to perform an audit of opening balances of the financial statements by a new auditor is outlined in the International Standard on Auditing (ISA) 510 Initial Audit Engagements – Opening Balances

The objective of audit opening balance

The objective of the auditor with respect to opening balances (OB) is to obtain sufficient appropriate audit evidence about whether:

1. The OB contain misstatements that materially affect the current period’s financial statements.

2. Appropriate accounting policies reflected in the OB that have been consistently applied in the current period’s financial statements or changes thereto are appropriately accounted for and adequately presented and disclosed in accordance with the applicable financial reporting framework.

The audit procedures

The auditor shall perform such additional audit procedures as are appropriate in the circumstances to determine the effect on the current period’s financial statements if the OB contain misstatements that could materially affect the current period’s financial statements.

General Audit Procedures

The auditor shall read the most recent financial statements including disclosures.

The auditor shall determine whether the prior period’s closing balances have been correctly brought forward to the current period or, when appropriate, have been restated.

The auditor shall obtain sufficient appropriate audit evidence to determine whether the opening balances reflect the application of appropriate accounting policies.

The auditor shall obtain sufficient appropriate audit evidence to review the predecessor auditor’s working papers to obtain evidence regarding the opening balances.

The auditor shall obtain sufficient appropriate audit evidence to perform specific audit procedures to obtain evidence regarding the opening balances.

Predecessor action

What can be done if the predecessor auditor does not, or cannot, provide access to the audit working papers for the previous reporting period?

The successor auditor should evaluate whether audit procedures performed in the current period provide evidence relevant to the opening balances, or perform specific audit procedures to obtain evidence regarding the opening balances, and propose opening balance adjustments, if necessary.

The auditor might want to recompute the allowance for doubtful debts accounts at the end of the prior period and compare original and recomputed numbers for consistency and reasonableness.

The auditor might want to review the property and equipment and its depreciation schedules for the prior year to compare them to the opening balances, as well as review the consistency of depreciation policies.

Source :

MIA Accountant Today

ISA 510 Opening Balances dated 14 January 2020

https://www.at-mia.my/2020/01/14/isa-510-opening-balances/

Visit Us

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

Website www.ktp.com.my

Instagram https://bit.ly/3jZuZuI

Linkedin https://bit.ly/3sapf4l

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

Website www.thks.com.my

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

Tiktok http://bit.ly/3u9LR6Q

Youtube http://bit.ly/3ppmjyE

Facebook http://bit.ly/3ateoMz

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

Instagram https://bit.ly/3u2PxHg

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Archive

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- November 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016